WHAT IS VAT?

Value Added Tax (VAT) for Real Estate in UAE is a tax imposed at the rate of 5% on properties including sale and tenancy contracts that can be supplied including but not limited to real estate.

WHAT IS A BUSINESS?

The business includes any activity conducted regularly, on an ongoing basis Independently by any person, in any location Including industrial, commercial, agricultural, professional, service or excavation activities or anything related to the use of tangible or intangible properties.

WHEN IS A REAL-ESTATE BUSINESS REQUIRED TO GET REGISTER FOR VAT?

- A Real Estate business having taxable supplies exceeding AED 375,000 is mandatorily required to get registered for VAT.

- A Real Estate business anticipates making taxable supplies with a value exceeding the mandatory registration threshold of AED 375,000 in the next 30 days.

- A Real Estate business can voluntarily register for VAT if its supplies are less than AED 375,000 and but exceeding the voluntary threshold of AED 187,500.

CHALLENGES IN REAL ESTATE BUSINESS

There are different challenges in VAT for real Estate such as:

- When to account for VAT in long-term contracts

- When I will get the payment

- Are invoices are currently issued for each rental payment

- How to apportion input tax on mixed-use developments

- Has the work actually been completed? Consideration of Transitional rules and certifications

VAT RELATED RESPONSIBILITIES OF A REAL ESTATE BUSINESS

Here a question is raised that what are the VAT related responsibilities of a real estate business? The answer is:

- All VAT registered businesses are required to keep accurate and updated financial record of all transactions and make sure that the financial record is reconciled with the VAT returns.

- For Real Estate Business, maintain accounting record generally for a period of 15 years.

- Businesses must ensure that their accounting software supports the accurate recording and reporting of VAT transactions.

- Businesses that do not qualify for the mandatory VAT registration threshold of AED 375,000 should maintain the VAT record to determine the event when they should register for VAT.

- Businesses must ensure that the VAT is charged on all sale and tenancy contracts

- Businesses may reclaim VAT they have paid on business-related purchases or tenancy contracts

- Submit the VAT return of all the supplies and payments on online portal of tax authorities not later than the 28th day following the end of the tax period.

WHAT IS A REAL ESTATE BUSINESS?

- Any area of land over which:

- Rights can be created

e.g. entitlement, authority, permission, or license to have or to do something in the area of land.

- Interests can be created

e.g. right, title or legal share can be created in the area of land.

- Services can be created

e.g. the work performed by someone in the area of land which is not even directly or indirectly owned by him.

- Any building, structure or engineering work permanently attached to the land.

e.g. It includes bridge, tower, pillar, Beam, Column, Frame, Trusses

- Any fixture or equipment which makes up a permanent part of the land or is permanently attached to the building, structure or engineering work.

e.g. lights, ceiling fans, cement, wall to wall carpeting, bookshelves etc.

- A supply of Services is deemed to relate to a real estate where the supply of Services is directly connected with the real estate, or where it is the grant of a right to use the real estate.

A supply of Services directly connected with real estate includes:

- The grant, assignment or surrender of any interest in or right over real estate.

- The grant, assignment or surrender of a personal right to be granted any interest in or right over real estate.

- The grant, assignment or surrender of a license to occupy land or any other contractual right exercisable over or in relation to real estate, including the provision, lease and rental of sleeping accommodation in a hotel or similar establishment.

- A supply of Services by real estate experts or estate agents.

- A supply of Services involving the preparation, coordination and performance of construction, destruction, maintenance, conversion and similar work.

WHAT IS A SUPPLY IN RELATION TO REAL ESTATE?

A supply of real estate may include the sale, lease or giving the right in any real estate.

WHAT IS CONSIDERATION IN RELATION TO REAL ESTATE?

Consideration is anything received in return for a supply. If the consideration is only money, the value of that supply is the amount of money received. Consideration is treated as VAT inclusive, so the amount received in payment includes an element of VAT for taxable supplies.

WHAT IS A RESIDENTIAL BUILDING FOR VAT PURPOSES?

A residential building is a building or part thereof that is intended and designed for occupation by individuals, and mainly includes buildings which can be occupied by any person as a main place of residence. It does not include the following:

- Any place that is not a building fixed to the ground and can be moved without being damaged.

- Any building that is used as a hotel, motel, bed and breakfast establishment or hospital etc.

- A serviced apartment for which services in addition to the supply of accommodation are provided.

- Any building constructed or converted without lawful authority

A residential accommodation is building intended and designed for human occupation including:

- A person’s principal place of residence

- residential accommodation for students or school pupils

- residential accommodation for armed forces and police

- orphanages, nursing homes, and rest homes

A residential building is not any of the following:

- Any place that is not a building fixed to the ground and can be moved without being damaged

- Any building that is used as a hotel, motel, bed and breakfast establishment, or hospital or the like

- A serviced apartment for which services in addition to the supply of accommodation are provided

- Any building constructed or converted without lawful authority

The provision of hotel accommodation will be subject to VAT at the standard rate, whereas the provision of residential accommodation will be exempt from VAT.

WHAT IS A COMMERCIAL BUILDING FOR VAT PURPOSES?

A commercial building is any building or part thereof that is not a residential building. Examples would be offices, warehouses, hotels, shops etc.

IS A RESIDENTIAL BUILDING SUBJECT TO VAT?

The first supply of a new residential building within the first three years of it being constructed shall be zero-rated. All subsequent supplies shall be exempt, even if within the first three years.

DOES THE OWNER OF REAL ESTATE HAVE TO REGISTER FOR VAT?

The owners of residential buildings do not have to register for VAT if they do not have any other business activities. Where owners have other business activities, they should consider their obligations further. The owner of any building that is not residential, will have to register if the value of the supplies over the preceding 12 months exceeds Dh375,000 or it is expected that they will exceed Dh375,000 over the coming 30 days.

CAN A REAL ESTATE OWNER RECOVER VAT PAID IN RELATION TO REAL ESTATE?

An owner of the residential building will not be able to recover VAT in respect of expenses related to the exempt supply of the residential buildings. An owner of a commercial building will generally be able to recover VAT in respect of expenses related to the supply of the building.

HOW IS A MIXED-USE BUILDING (RESIDENTIAL AND COMMERCIAL) TREATED FOR VAT?

The rent or sale of a residential part of the building shall be treated as zero-rated or exempt, depending on whether this is a first supply or a subsequent supply. The rent or sale of a commercial part of the building shall be treated as subject to VAT at 5%.

The tax incurred by the owner on the building needs to be apportioned where there is an exempt supply, and the portion related to the taxable supply (at 0% and 5%) may be recovered.

WILL VAT BE CHARGED ON THE PROPERTY I AM RENTING?

The rent of residential building will generally be exempt from VAT. The rent of commercial building will be subject to VAT at 5%.

Place of Supply

Place of supply of real estate services is the location of the real estate.

EXAMPLE 1:

Cross-Border B2B Supply of Real Estate Services- Services Supplied Where the Real Estate Is Located

Oman & Co. supplies UAE land related services to KSA & Co, Place of supply: UAE (where the building is located), Oman & Co has to register in the UAE and account for UAE VAT.

EXAMPLE 2:

Inbound Real Estate Services Supplied B2B To A Customer In The UAE.

UK Co supplies architect services to UAE Co which relates to a specific building in the UAE. UK Co does not charge VAT because UAE Co is VAT registered. UAE Co remits 100 AED to UK Co. UAE Co accounts for VAT under the reverse charge mechanism.

EXAMPLE 3:

Lease of UAE Real Estate By A Non-UAE Landlord

UK Co leases a building in UAE to UAE Co. The building may constitute a fixed establishment in the UAE.UK Co has to register in the UAE and account for UAE VAT.

WHEN TO ACCOUNT FOR OUTPUT VAT ON SUPPLIES?

For goods:

- Date of removal of goods (in case of supply of goods with transportation)

- Date on which goods made available to the customer (in case of supply not involving transportation)

- Date of assembly/ installation (supply of goods involving assembly or installation)

For Services

- Date on which performance of service is complete

Basic Tax Point

- Receipt of payment or the date of a VAT invoice if earlier than the basic tax point

CONTINUOUS SUPPLIES & STAGE PAYMENTS

- The earlier of receipt of payment, the due date of payment shown on the VAT invoice or the date of the VAT invoice

EXAMPLE 1:

- Building material issued to the customer– 01 February 2018

- Invoice issued- 01 March 2018

Date of Supply: The date when building material is issued to the customer- 01 February 2018.

EXAMPLE 2:

- 1st payment for construction work- 01 January 2018

- 2nd payment for construction work- 01 February 2018

- Invoice issued relating to payments 1 and 2- 03 March 2018

Date of Supply: 01 January 2018 and 01 February 2018.

EXAMPLE 3:

- Payment received from the customer– 02 February 2018

- Service started– 02 March 2018

- Service completed– 02 April 2018

Date of Supply: 02 February 2018.

EXAMPLE 4:

- 1st part of construction work is completed– 01 February 2018

- Construction completed and payment is made– 01 March 2018

Date of Supply: 01 March 2018. Under transitional rules, VAT is due on the value related to the construction work completed after the implementation of VAT.

VAT IMPLICATIONS ON SUPPLIES OF LAND AND REAL ESTATE

It is classified into three types:

-

STANDARD RATED

- Lease or sale of commercial property

- Car parking and hotels

-

ZERO RATED

- First supply of residential buildings within 3 years of its completion

- First supply of Charity related buildings

- First supply of buildings converted from non-residential to residential

-

EXEMPT

- Supply of residential buildings

- Bare land

SHORT TERM LEASES

However, the supply of residential accommodation will only be exempt from VAT where:

- The duration of the lease exceeds 6 months; or

- The tenant of the property holds an Emirates ID

- If the duration is up to 3 months and no emirates ID then VAT will be charged @5%.

CAPITAL ASSETS SCHEME

- Adjustment of VAT recovery on costs incurred relating to large value capital assets with a long useful life

- Intended to reflect the use of the asset for taxable or exempt purposes over its useful life–intended use of the asset may change over time and VAT recovery based on intended first use may not fairly reflect its use over time

WHAT?

Qualifying assets > 5,000,000 AED on which VAT was payable:

- building or a part thereof: useful life > 120 months

- other than building or parts thereof (e.g. computer): useful life > 60 months

ON WHAT PERIOD?

- building or a part of a building –10 years

- Assets other than a building –5 years

CAPITAL ASSETS SCHEME –ADJUSTMENT CALCULATION

Year 1: recover input tax incurred on the purchase of the asset based on the expected taxable use of the asset e.g. 100% taxable use, therefore recover all input tax incurred in full.

Year 2 –10: adjust input tax recovery for that year based on that year’s taxable use e.g. total input tax incurred / 10 years = input tax for year 2 x difference between initial recovery percentage and actual taxable use.

Total input tax on capital/Adjustment Period X Original taxable use%- Actual taxable use% = Additional VAT recoverable from FTA /additional VAT payable to FTA.

CAPITAL ASSETS SCHEME: EXCLUSION FOR NEW RESIDENTIAL BUILDINGS

- Where the first supply of a residential property is a zero-rated lease, the costs incurred in relation to that property can be deducted in full- directly attributable to the first zero-rated supply.

- This rule applies regardless of an intention to make future exempt supplies of the property e.g. second supply of a residential property by way of lease or sale.

- As a result, there is no need to apply the capital assets scheme in such circumstances.

TRANSFER OF A GOING CONCERN

A property rental business can be a Transfer of a Going Concern where it is transferred along with all of the components necessary to make it a business. This could include:

- Continuing lease contracts with tenants

- Staff required to operate the business

- The property required to operate the business

- Contracts necessary to operate the business

INPUT TAX RECOVERY “DIY HOUSE BUILDERS” SCHEME

This is a scheme set up to allow individuals building their own residence to reclaim VAT spent on building materials and some other services- intended to put a person in the same VAT position as if they had purchased a newly completed residential building i.e. VAT would apply to that purchase at 0%.

What Can Be Deductible?

- Input VAT relating to the construction of a person’s residence or the residence of their family

- Input VAT incurred on contractor’s services e.g. builders, architects, engineers etc. and building materials (not including e.g. furniture and appliances other than fitted furniture and appliances etc.

Who

- An individual who is a National of the UAE

How

- By submitting a refund claim to the Tax Authority within 6 months from the date of the completion of the newly built residence.

- A claim may not be made in connection with a building that the person intends to sell or lease to someone else within a period of two years of its construction.

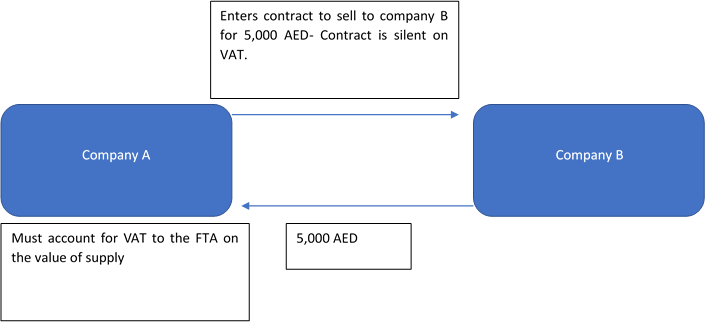

TRANSITIONAL RULES- CONTRACTS

Where a contract is entered into prior to the effective date of the VAT law which concerns a supply made wholly or partly after the effective date of the VAT law, VAT will be due on the supply taking place after the effective date of the VAT law.

If the contract does not mention VAT, the value of the supply stated in the contract shall be treated as inclusive of VAT.

TRANSITIONAL RULES – CONTRACTS

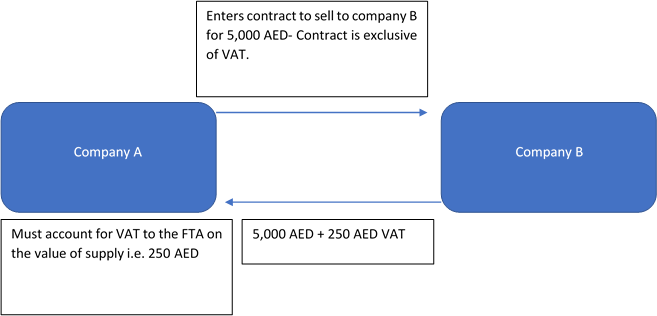

However, where Company B is registered for VAT and is entitled to full VAT recovery on costs incurred, Company A can treat the contract as if the price stated was exclusive of VAT and is able to charge VAT to Company B in addition.

TRANSITIONAL RULES – EARLY INVOICING OR PAYMENTS

Where an invoice is issued or payment is received prior to the date the VAT Law comes into effect, the value of the payment/invoice will be subject to VAT where the following takes place after the date the VAT Law comes into effect:

- Transfer of goods under the supplier’s supervision

- Goods are placed in the possession of the recipient of the goods

- Completion of an assembly of the goods

- A customs statement is issued

- The customer accepts the supply of goods

The rules above are intended to avoid invoices being issued or payments being made prior to the effective date of the VAT law for supplies of goods which effectively take place after the effective date of the VAT law, for the purposes of avoiding tax.

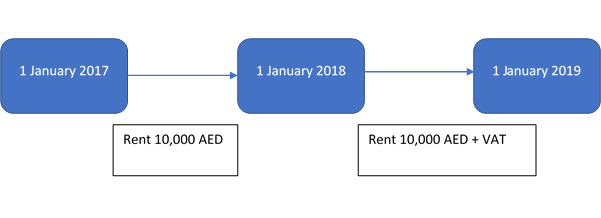

TRANSITIONAL RULES- REAL ESTATE

Contracts for the rental of real estate which span the VAT implementation date will be treated as subject to VAT to the extent the value payable relates to the rental which took place after the effective date of the VAT law.

CONVERSION OF PROPERTY FROM COMMERCIAL TO RESIDENTIAL

In the case of buying a commercial building and converting it into a residential building, the buyer is entitled to recover the tax paid within a period of three years from the date of transfer. The same applies if the customer rents a residential property that has been built. As for mixed-use buildings, the residential part is subject to the exemption or zero rates according to its percentage of the building, while the commercial part is subject to tax.

The sale of vacant commercial properties or the off-plan sale of commercial properties under the building license is subject to a 5 percent VAT; however, the tax paid during the lease period can be recovered through the tax return of the tenant if they are a taxable person registered for tax purposes and entitled to a tax refund. Tax paid towards the purchase of an entire building may be recovered according to the capital asset scheme if the cost of the property exceeds Dh5 million.