Economic Substance Regulations | [ESR]

The United Arab Emirates introduced in April 2019 a legislation named as Economic Substance Regulations [ESR]. For many Years UAE has been considered as a Tax Haven by the many entities due to its lack of direct and indirect taxes.

Recently, however, the United Arab Emirates has introduced legislation to tax supplies in its jurisdiction termed as a Value Added Tax [VAT]. The introduction of Economic Substance Regulations [ESR] is one of the many ways in which the United Arab Emirates has aligned its policies with that of the Organization for Economic Cooperation and Development [OECD]. The directives issued by the Organization for Economic Cooperation and Development [OECD] for BEPS [Base Erosion Profit Shifting] are a direct precursor of Economic Substance Regulations [ESR] directives.

Base Erosion Profit Shifting directives are regulations issued by the Organization for Economic Cooperation and Development [OECD] to combat corporate policies for Tax Planning which would shift the profits of companies from low tax rate jurisdictions to high tax jurisdictions. Thus “eroding” the tax base in high tax jurisdictions.

Commitment to the Organization for Economic Cooperation and Development [OECD] requirements and being a member country of the same body, UAE has introduced the ESR. The issuance of ESR has also helped the UAE to comply with the assessment of UAE Tax Frameworks made by the European Union.

The purpose of the ESR is to bring specific requirements for businesses to demonstrate actual activity in the UAE. With the introduction of ESR, UAE has been removed from the blacklist of tax havens.

The ESR adopted by the UAE is roughly similar to the regulations of the Organization for Economic Cooperation and Development [OECD] member countries which have a similar tax structure as the United Arab Emirates.

The Economic Substance Regulations [ESR] require all UAE entities, whether they are onshore, free zone, branch or representative offices that undertake one or more “Relevant Activity” for Financial Year commencing on or after January 2019.

It should be noted that Entities that direct or indirect ownership amounting to 51% of its total shares is exempted from the compliance requirements of ESR. All UAE Entities need to whether and which of their activities fall within the scope of the Economic Substance Regulations, as well as ensuring that they meet the requirements in respect in each relevant activity. This is in essence both a qualitative and quantitative assessment that would involve consideration of operational, financial, tax/transfer pricing, legal, and governance matters.

What are the relevant activities for Economic Substance Regulations [ESR] Compliance Requirements?

The regulations will apply to companies and other business forms which are registered within the UAE mainland, Free Zones, and Financial Free Zones, that carry out the following activities:

- Banking Business

- Insurance Business

- Investment Fund Management Business

- Lease Finance Business

- Headquarters Business

- Shipping Business

- Holding Company Business

- Intellectual Property Distribution Business

- Distribution and Service Centre Business

It should be noted with clarity that there is a requirement for a business to use the “Substance over Form” approach when evaluating whether they undertake a relevant activity or not.

This means that companies will not only be evaluated on what activities are stated on their commercial license but their activities will be evaluated and ESR applied accordingly. It is not a requirement that a UAE entity is directly engaged in the performance of a relevant activity directly. If an entity is earning income passively from a relevant activity, it will be sufficient for the application of Economic Substance Regulations [ESR].

What are the requirements for UAE Entities for Economic Substance Regulations [ESR]:

All Entities which assess that they are involved in the performance of a Relevant Activity will carry out the Economic Substance Test for Economic Substance Regulations [ESR]. The Economic Substance is composed of two parts:

- The Direct and Managed Test:

- The Entity needs to be directed and managed in the UAE with regards to the relevant activity carried out in the Emirates.

- The Core Income Generated Activities Test [CIGA]:

- The Entity that performs the relevant activities for the purpose of application of Economic Substance Regulations [ESR], need to demonstrate that the CIGA’s are undertaken in the UAE.

- The activity which constitutes as a CIGA varies with the activity being performed.

Below is a list of CIGA activities for each relevant activity, however, the list is for illustrative purposes and is not exhaustive.

| Relevant Activities | Examples of CIGA |

|

Banking |

§ Raising Funds

§ Managing Risks § Taking Hedge Positions § Providing Loans, credit and other financial services § Managing Capital and preparing reports to investors.

|

|

Insurance |

§ Predicting and Calculating Risk

§ Insuring and Re-insuring against the risk § Providing Insurance business services § Underwriting Insurance and Re-insurance

|

|

Investment Fund Management |

§ Taking Decision on holding and selling of investments

§ Calculating risk and reserves § Taking decision on currency or interest fluctuations § Preparing report for Investors |

|

Lease Finance |

§ Agreeing Funding Terms

§ Identifying and acquiring assets to be leased. § Setting terms and duration of any leasing § Monitoring and revising agreements § Managing risks |

|

Headquarters |

§ Taking relevant management decisions

§ Incurring operating expenditures § Co-ordinating Group Activities |

| Holding Company | § All activities related to the business that derives income from dividends and capital gains from equity interest |

|

Shipping Company |

§ Managing crew

§ Overhauling and Maintenance of ships § Overseeing and Tracking Shipping § Determining what goods to order and when to deliver. § Organizing and overseeing voyages. |

|

Intellectual Property |

§ Taking a strategic decision and managing principal risks related to the development and subsequent exploitation of intangible assets generating income. Acquisition by third parties and subsequent exploitation and protection of the intangible assets. |

|

Distribution and Service Center |

§ Transportation and storing component parts.

§ Material and goods ready for Sale § Managing Inventories § Taking Orders § Providing Consulting and Other Administrative Services |

What are Economic Substance Regulations [ESR] Reporting Requirements?

The Entities which exist in the United Arab Emirates and carry out relevant activities within its jurisdiction need to follow certainly and comply with certain reporting requirements.

The entities will be required to submit an annual notice to their Regulatory Authority indicating that they are carrying out a Relevant Activity in the preceding Financial Year and whether there has been any Income from the Relevant activity that has been subject to Taxation outside the United Arab Emirates.

It should be noted that UAE entities that qualify for an exemption from the Economic Substance Regulations, or those that did not earn any income from their Relevant Activities will still be required to file a notification with the Relevant Authority.

UAE Entities which qualify for submission of notification and those that earned any income from the same will also be required to file an Annual Economic Substance Return. The purpose of the Return will be to make an assessment of the requirements of economic substance regulations are met, the income earned, qualifications of the staff involved, and information about the premises and other assets used in carrying out the relevant activity.

What are compliance timelines for [ESR]?

The question arises as to when the entities which are required to comply with Economic Substance Regulations [ESR]. For understanding this, we can divide the requirements into two categories:

- Existing Entities:

These entities must comply with the requirements of the regulations from the beginning of their financial year commencing on or after the 1st of January 2019. The first Return for these entities will be due 12 months after the financial year ends in 2020. For entities engaged in relevant activities with a calendar year ending by the year 31 December, the first notification and return need to be submitted by 31st of December 2020.

- New Entities:

New Entities that are engaged in carrying out the relevant activities must comply with the regulations from the commencement of the Financial Year. The first return due will be after their Financial year-end [could be in the year 2020 or later]

What are the Penalties for Non-Compliance of [ESR]?

In addition to an exchange of information by the UAE with countries which are a member of Organization for Economic Cooperation and Development [OECD] to remove the possibility of Base Erosion and Profit Shifting, failure to comply will cause the levy of administrative penalties not less than 10,000 AED and not more than 50,000 AED for failure to comply for the first year. In case of failure to comply with ESR, the minimum amount of penalty will be increased to 50,000 AED and the maximum amount to 300,000 AED.

In addition to this, additional penalties, such as suspending, revocation of UAE Trade License may also be levied.

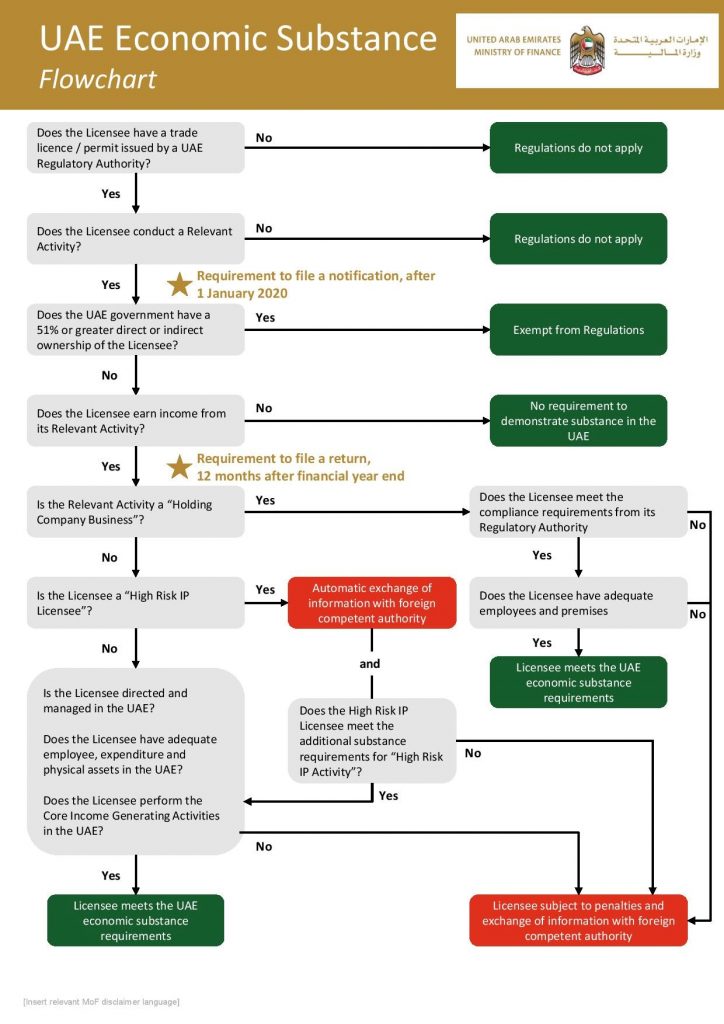

Summary for Economic Substance Regulations [ESR] Compliance:

For better understanding, the following flow chart will better explain the application of Economic Substance Regulations [ESR].