Value Added Tax (VAT) In the United Arab Emirates

Frequently asked questions (Construction Industries) and (Value Added Tax)

Impact on Construction Industries

Impact on Construction Industries

CONSTRUCTION CONTRACTS

VAT ON EXISTING CONSTRUCTION CONTRACTS:

Q: How will your current construction contract deal with the introduction of VAT?

A: Under the Contract, the contractor is obliged to pay all taxes as required under the law and thus the contract price is deemed to include these taxes and duties based on the rates applicable at the ‘Base Date.’ However, there are provisions in the Contract that allow a contractor to claim an increase in costs due to a change in the laws of the country where the permanent works are being executed.

Q: Where the supplier supplies goods after the implementation date but has received the payment before the effective date?

A: Those transactions come under the purview of the Value Added Tax. Even if the trade happens before the effective date but does not have the clause of tax, then it comes under VAT.

VAT (VALUE ADDED TAX) ON FUTURE CONSTRUCTION CONTRACTS:

Q: Construction contracts post January 2018?

A: The importance of construction contracts stating whether or not VAT is payable on top of the contract price was considered. In the absence of the contract price not stating it is exclusive of Value Added Tax the contract price is deemed inclusive of Value Added Tax. VAT will impact the contract price in construction contracts. Going forward, employers and contractors should be clear as to whether the VAT is to be paid on top of the tender price or if it is included in the Contract Price.

Q: What will be the impact of VAT on construction cost?

A: Majority of contractors and developers will offload Value Added Tax costs to the end user, not all Value Added Tax will be recoverable, which will lead to a modest increase in construction costs.

Q: What will be the impact of non-registration of sub-contractors of the Construction companies?

A: In particular, larger construction companies may not be entitled to recover Value Added Tax from smaller subcontractors who are not registered for Value Added Tax or fall below minimum threshold requirements. In such instances, the cost borne by the construction supply chain will lead to higher construction costs.

GENERAL FLOWCHART OF VAT (VALUE ADDED TAX) IMPLEMENTATION

Q: What will be major construction challenges after incorporating the VAT?

Lead Times:

Lead times are common in most demand led industries, but in the case of major construction projects, they can be extremely long. It is almost certain that a large number of the major projects due to be delivered over the next few years will not have had VAT factored into them, either on the cost or revenue side. To some extent this was inevitable; the gestation of the VAT project in the region has been somewhat erratic to a number of observers and some businesses have planned for that status quo to remain for some time. Clearly, that is no longer the case. The issue associated with the duration of contracts drawn up in the sector is that many will not, at the time of drafting, have included any of the normal terms and conditions relating to VAT which one would ordinarily expect in jurisdictions where the tax has been implemented.

Contract Price:

For the contractor in such instances, will they be in a position to charge VAT in addition to their normal contract price? On the face of it this appears to be a simple question, but in reality, it is often not. Payment for VAT purposes is generally considered to be inclusive of VAT. That means that in our case the contractor will need to agree with their customer that they can charge VAT in addition to the price previously agreed in order to avoid the charge becoming a cost they have to bear themselves. Bearing in mind that contracts in the region are generally struck on a tax-inclusive basis, making this change may not be as straightforward as one would hope, regardless of the position of the customer vis a vis VAT recovery.

Contract Pricing of Future Projects:

Furthermore, from a pricing standpoint, it is unlikely that the market (after the introduction of VAT) would simply reprice itself to cover the VAT charge in full. Indeed, customers may well look to their suppliers to cover some of the VAT charges themselves anyway. There may well be some sort of a transitional regime granting suppliers the right to “grandfather” existing tax-inclusive contracts into the new VAT environment.

However, whilst such approaches have been seen elsewhere, it remains to be seen whether that would be the case in the GCC. This is, therefore, a major area of potential risk for any contracts agreed before the implementation of VAT but which will be executed or delivered after, the purchaser and vendors are unlikely to simply concede their respective positions easily given the cost of VAT must fall on one of them.

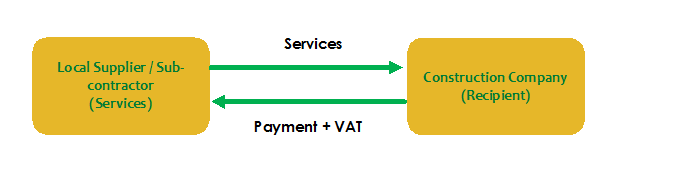

Taxation of Local Services and Goods

Taxation of Local Services and Goods

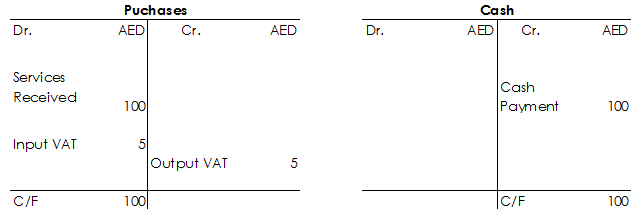

Q: What will be VAT treatment of a local supply of services to construction company?

A: Where Construction company receives a supply of services from a local service provider in the UAE, and the Local supplier will charge for the services plus VAT to the construction company in tax invoice;

The construction company may claim the VAT charged by the supplier/subcontractor in its tax return if it receives a valid tax invoice and payment is made within 6 months. Input tax may, however, be blocked if services relate to entertainment or employee private use per Article 53 of the Executive Regulations.

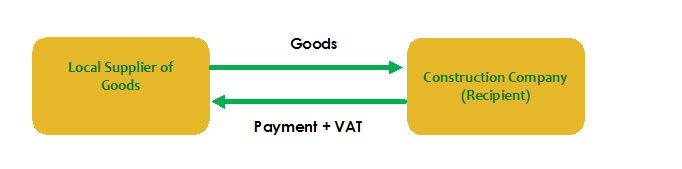

Q: What will be VAT treatment of a supply of goods from local supplier to construction company?

A: Construction company can deduct the VAT charged by the supplier in its tax return, provided the VAT is not blocked by the exceptions listed in Article 53 of the Executive Regulations if:

• A valid tax invoice is obtained; and

• The tax invoice will be paid in 6 months.

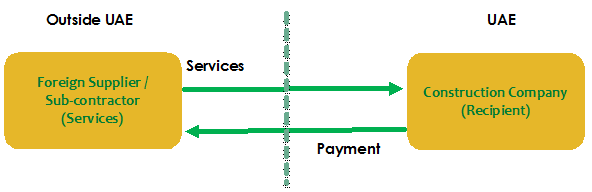

Taxation of Imported Goods and Services

Taxation of Imported Goods and Services

Q: What will be VAT treatment of a supply of services from outside the UAE to construction company?

A: Where Construction company receives services in UAE from outside the UAE and is charged for the service, as outlined in the diagram below. The services will be regarded as being supplied to UAE regardless of whether the foreign office of the Construction company procured and pays for the services.

CA construction company will have to self-account for VAT on the imported service and adjust its tax position using the Reverse Charge Mechanism on its tax return.

Q: What will be VAT treatment of a supply of goods from outside the UAE to construction company?

A: Where Construction company imports goods in UAE from outside the UAE, as outlined in the diagram below. The goods will be regarded as being supplied to UAE regardless of whether the foreign office of the Construction company procured and pays for the goods.

A construction company will have to self-account for VAT on the imported goods and adjust its tax position using the Reverse Charge Mechanism on its tax return.

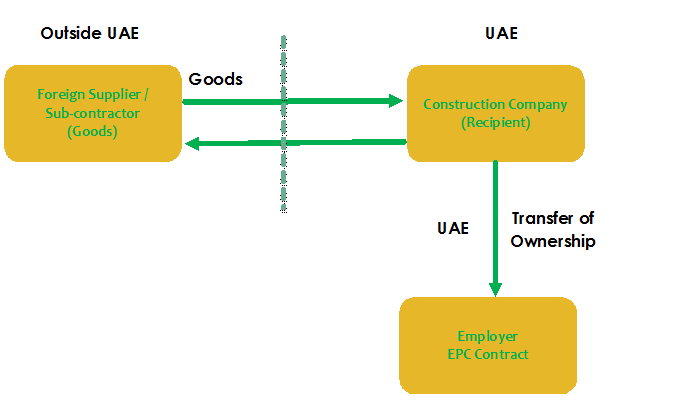

Q: What will be VAT treatment of a supply of goods from outside the UAE to a construction company in UAE and ownership is transferred to the Employer?

A: In the case where Construction company transfers the ownership of goods received from a non-UAE supplier to Employer, upon the transfer of the goods to the transport vessel.

In such case, Employer generally will be the importer on record for customs purposes, and Construction company will use these goods for the purposes of the construction of the site.

Misc. Consideration related to VAT (Value Added Tax)

Misc. Consideration related to VAT (Value Added Tax)

REIMBURSEMENT OF COST INCURRED BY EMPLOYEES:

Q: What will be the treatment of cost incurred by the employees, and thereafter reimburse by the construction company?

A: From a VAT perspective, there is always a risk that where the employer has not incurred the expense directly, that the employer may not have a right to recover the associated VAT on the expense (whilst reimbursing the employee for the cost plus local VAT).

Therefore, try to ensure that invoices are made out to its legal name instead of being addressed solely to the employee and valid tax invoices are collected. Furthermore, input tax related to entertainment is irrecoverable, unless the requirements of Article 53 of the Executive Regulations are met, i.e. there must be a contractual obligation or documented policy to provide those services or goods to those employees in order that they may perform their role and it can be proven to be normal business practice in the course of employing those people.

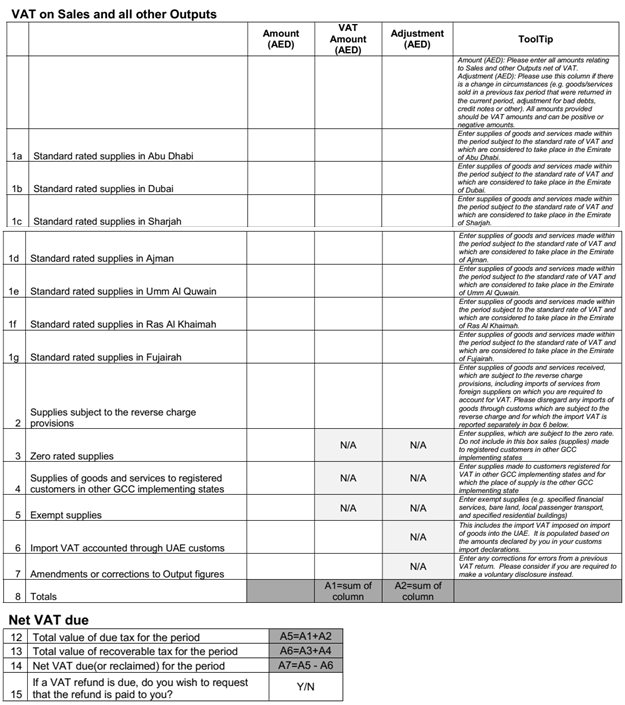

VAT RETURN FILLING REQUIREMENTS:

Q: When are registered businesses required to file VAT returns?

A: Taxable Persons must file VAT returns with the FTA on a regular basis, within 28 days of the end of the Tax Period, which shall be:

• Quarterly for businesses with an annual turnover below AED150m

• Monthly for businesses with an annual turnover of AED150m or more.

The Tax returns shall be filed online using services.

Q: What will be the length of tax period for filing of tax returns?

A: The standard Tax Period applicable to a Taxable Person shall be a period of three calendar months ending on the date that the Authority determines.

Q: What will be the last date of payment of tax to authority?

A: A Tax Return must be received by the Authority no later than the 28th day following the end of the Tax Period concerned or by such other date as directed by the Authority

Q: What will be treatment where tax recoverable exceeds from tax due to authorities?

A: Where Recoverable Tax for a Tax Period exceeds Due Tax for the Tax Period, the excess Recoverable Tax may be repaid to the Taxable Person in accordance with the relevant provisions in the Decree-Law and the Federal Law No. (7) of 2017.

VAT (VALUE ADDED TAX) RETURN FORMAT:

Read more about VAT For Real Estate in UAE